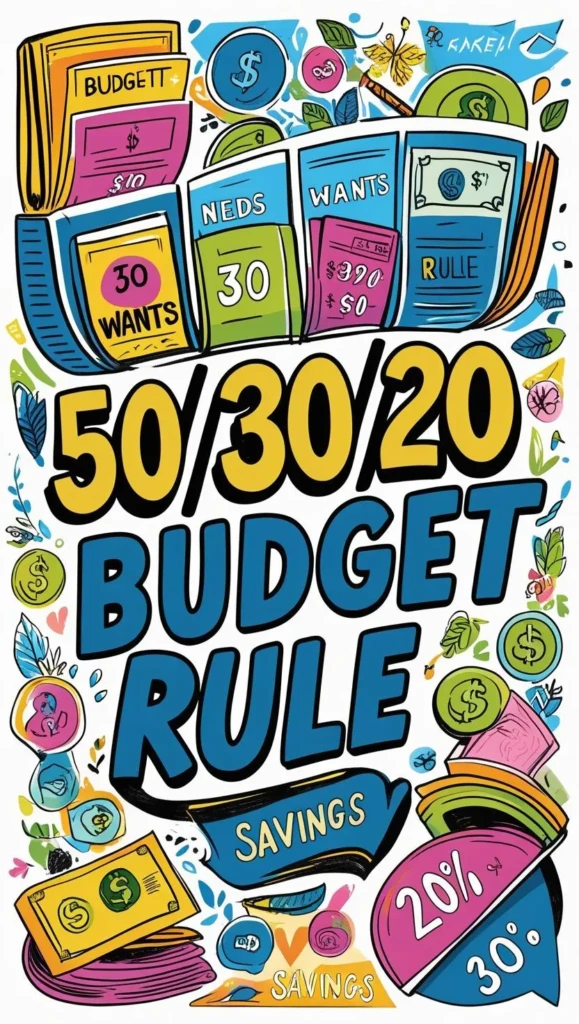

You may have heard about the 50/30/20 budget rule floating around personal finance circles, but let’s be honest—most individuals mess it up within the first month. I certainly did when I first tried it three years ago, blowing through my “wants” category by day 15 like it was Black Friday. The thing is, this isn’t just another budgeting fad that’ll leave you frustrated and broke. When you actually master these nine strategies, something pretty remarkable happens to your financial stress levels.

Key Takeaways

- Track every expense for three months to identify spending patterns and accurately calculate your real take-home pay.

- Automate essential payments like rent and utilities, then automatically transfer 20% of income to savings accounts.

- Adjust the 50/30/20 percentages based on your situation—high debt, children, or expensive cities may require modifications.

- Use budgeting apps like Mint or YNAB to automatically categorize expenses and set spending alerts for each category.

- Rebalance monthly by assessing whether your current split matches your lifestyle needs and future financial goals.

Track Your Spending for Three Months to Understand Your Financial Patterns

Before you plunge into the 50/30/20 budget rule, you need to figure out where your money’s actually going – and trust me, the reality might surprise you. Track every single expense for three months, because that’s when patterns emerge. You’ll spot your fixed costs like rent, variable expenses like groceries, and those sneaky seasonal splurges.

During this financial detective work, categorize everything into three buckets: needs, wants, and savings. This matches perfectly with the 50/30/20 framework you’re about to master. Three months gives you enough data to see trends without getting overwhelmed by analysis paralysis.

Your income stays consistent, but your spending habits reveal the real story. Understanding these patterns puts you in control of creating a budget that actually works. Use accounting software to track your income and expenses systematically, which will make monitoring your financial patterns much more efficient and accurate.

Calculate Your True After-Tax Income Before Setting Categories

The foundation of any successful 50/30/20 budget starts with knowing your real take-home pay, not that inflated number on your job offer letter. Your true after-tax income is what actually hits your bank account after taxes, insurance, and retirement contributions disappear into the void.

I learned this lesson when I tried budgeting with my gross salary and wondered why I couldn’t make ends meet. Track your actual paychecks for three months to account for overtime fluctuations and quarterly bonuses. This precision gives you the power to properly divide your income into three categories: 50% for needs, 30% for wants, and 20% toward savings and debt repayment.

Just like a business needs detailed financial projections to stay on track, your personal budget requires accurate income calculations to guide your spending decisions. Accurate budgeting means building an emergency fund that actually works, not fantasy math.

Identify and Prioritize Your Non-Negotiable Essential Expenses

Once you’ve nailed down your real take-home pay, it’s time to face the brutal reality of your essential expenses—those sneaky little costs that’ll hunt you down whether you budget for them or not.

These living expenses are necessary for survival and absolutely can’t be ignored. Here’s what you’re dealing with:

- Housing costs – Your rent or mortgage payments typically eat up the biggest chunk

- Utility bills – Electricity, gas, water, and internet keep your world spinning

- Food and groceries – Because surviving on air isn’t really an option

- Transportation costs – Car payments, insurance, and fuel for daily living

- Healthcare expenses – Insurance premiums and medical bills protect your future

You’ll want to budget to make sure these get covered first, before anything else touches your money. If your essential expenses are consuming too much of your budget, consider exploring small business ideas that can help generate additional income to better balance your financial priorities.

Automate Your Savings and Bill Payments for Consistency

Frankly, your brain wasn’t designed to recall 15 different due dates while calculating exactly how much to transfer into savings each month—and that’s where automation becomes your financial superhero.

Start budget using automatic transfers to move 20% of your paycheck directly into your savings account before you even see it. Set up autopay for your must pay bills like rent and utilities, so you’ll never face late fees again.

A good budgeting app links your bank account and tracks your income and expenses automatically, making your monthly budget practically manage itself. You can adjust as needed, but automation handles the heavy lifting consistently.

Take automation even further by using app automation tools to connect your banking app with your budgeting software, creating seamless workflows that update your budget categories without manual data entry.

Adjust the Percentages Based on Your Personal Financial Circumstances

While automation keeps your budget running smoothly, you’ll quickly discover that the classic 50/30/20 split doesn’t fit everyone’s reality like a one-size-fits-all t-shirt. Your personal circumstances demand a customized approach to achieve true financial freedom.

Take advantage of this budgeting method’s flexibility by adjusting percentages to match your unique situation:

- High-cost living areas: Bump needs to 60-65% while reducing wants to accommodate rent that’d make your credit card weep

- Heavy debt load: Shift 10-15% from wants to debt repayment for faster financial goals achievement

- Parents with kids: Increase needs percentage for childcare costs that rival mortgage payments

- Irregular income: Create buffer zones within each category for those feast-or-famine months

- Aggressive savers: Reduce wants to 20% and boost savings goals to 30%

Consider starting a home-based business to supplement your income and create additional flexibility within your budget categories. This Budget Rule becomes your personalized financial plan when you manage your money strategically.

Build Your Emergency Fund Before Focusing on Other Savings Goals

Before you start dreaming about that shiny new investment portfolio or exotic vacation fund, you need to build your emergency fund first – it’s like putting on your financial seatbelt before hitting the road. Your emergency fund should cover three months of living expenses minimum, though six months gives you real power over unexpected expenses like car repairs or job loss.

Calculate your monthly net income and work toward saving that amount multiplied by three. I’d recommend opening a separate savings account specifically for emergencies – trust me, you’ll be tempted to raid it otherwise. Your financial situation will thank you when life throws curveballs.

Once you’ve got this foundation, then you can focus on other exciting savings goals within your budget. Having this financial cushion is especially crucial if you’re considering entrepreneurial ventures, as bootstrapping with personal savings requires a solid emergency buffer to minimize risk while building your business gradually.

Review and Rebalance Your Budget Categories Monthly

Once you’ve got your emergency fund locked and loaded, your budgeting journey doesn’t end there – it actually gets more interesting because you’ll need to check in with your 50/30/20 split every month. This isn’t busywork – it’s how you stay in control of your financial future and make smart money management decisions.

Monthly budget check-ins aren’t busywork – they’re your power moves for staying in control of your financial future.

Here’s your monthly budget power move:

- Review your budget against your monthly after-tax income to spot any drift

- Adjust the percentages when life throws curveballs at your spending patterns

- Reallocate funds between your categories: 50% for needs, 30% for wants, 20% for savings

- Assess whether your current split still matches your lifestyle and future needs

- Rebalance proactively to maintain discipline around the things you need versus want

These decisions you make monthly determine everything. Remember to see money as a tool during these reviews – successful women make confident decisions about their finances and learn from any adjustments they need to make along the way.

Find Creative Ways to Reduce Wants Without Feeling Deprived

The hardest part about cutting your “wants” spending isn’t finding places to trim – it’s doing it without feeling like you’re living on rice and beans while everyone else enjoys life. Use a budget calculator to track your wins, then celebrate when you hit your 30% wants target without going overboard.

You’ll find it easier to save money when you create clear guidelines for splurges versus skips. Try setting aside $50 monthly in your checking account for guilt-free treats, whether you live in an area with expensive entertainment or not.

Smart budgeting systems help you enjoy life while building wealth – pack that lunch, hunt those sales, and negotiate those bills like the financial boss you’re becoming. Consider incorporating simple self-care practices like gratitude journaling to help you appreciate what you already have and reduce the urge to overspend on wants.

Use Technology and Apps to Monitor Your 50/30/20 Allocation

Juggling three budget categories in your head while standing in Target’s dollar section is like trying to solve calculus during a fire drill – theoretically possible, but you’re probably gonna mess it up.

Smart technology divides your after-tax income into three categories automatically, putting money aside without the mental gymnastics.

Here’s how to leverage services offered by top budgeting platforms:

- Mint, YNAB, and PocketGuard automatically categorize expenses and track your three main budget allocations

- Google Sheets templates visualize where your income toward each category actually goes

- Automatic transfers move funds to separate accounts for retirement and savings

- Linked bank accounts simplify expense tracking across all spending categories

- Spending alerts help you stay within limits, even with high cost of living pressures

Remember, the best productivity system is the one you’ll actually use consistently, so start simple and only add complexity when you truly need it.

Let technology handle the math while you focus on financial domination.

Conclusion

You’ve got the tools to make the 50/30/20 rule work for your life, not against it. Start tracking today, automate what you can, and don’t beat yourself up if you mess up the first month – I certainly did. The key is consistency, not perfection. Adjust the percentages when life throws curveballs, review monthly, and celebrate small wins. Your future self will thank you for starting now.

In today’s world, starting a business doesn’t have to break the bank. I believe that wit

As a woman who loves reading, I’ve found many inspiring books written by other women. Here&rsq

Getting a $500k house requires more than good credit—discover the 6 steps most buyers miss that ke

Leave a Reply